Understanding Whole Life Insurance: Benefits and Features Explained

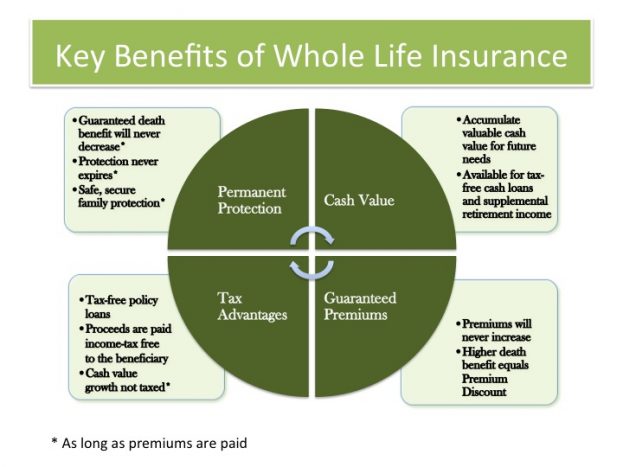

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as premiums are paid. Unlike term life insurance, which covers the policyholder for a specified time period, whole life insurance combines a death benefit with a savings component known as cash value. This cash value grows at a guaranteed rate and can be borrowed against or withdrawn during the policyholder's lifetime, making it a versatile financial tool. Understanding the benefits of whole life insurance is crucial for anyone considering this option as part of their long-term financial planning.

One of the main benefits of whole life insurance is the stability it provides. Policyholders can enjoy predictable premiums and a guaranteed death benefit, making it easier to manage long-term financial plans. Furthermore, because the cash value accumulates over time, it can serve as a financial safety net, offering liquidity for emergencies or future investments. Additionally, the interest earned on the cash value is tax-deferred, which can enhance the overall growth of your investment. Overall, whole life insurance not only offers peace of mind with lifelong coverage but also provides a savings vehicle that can contribute to financial stability.

Is Whole Life Insurance the Right Choice for Your Financial Goals?

When considering whole life insurance, it's essential to assess how it aligns with your overall financial goals. Unlike term life insurance, which only provides coverage for a set period, whole life insurance is a permanent solution that also accumulates cash value over time. This dual benefit can serve as a financial tool for various purposes, such as supplementing retirement income, funding a child's education, or acting as an emergency savings account. Additionally, the cash value grows at a guaranteed rate and can be accessed through loans or withdrawals, making it a versatile option for long-term planning.

However, before opting for whole life insurance, it's crucial to evaluate your specific needs and circumstances. Whole life insurance typically comes with higher premium payments compared to term policies, which may not be suitable for everyone, especially those on a tight budget. Consider creating a financial roadmap that includes factors like your current savings, debt obligations, and long-term objectives. Consulting with a financial advisor can also provide valuable insights into whether this type of insurance fits into your broader financial strategy or if other investment options might better serve your goals.

How Whole Life Insurance Can Serve as a Wealth-Building Tool

Whole life insurance is commonly viewed as merely a safety net for loved ones in the event of an untimely demise; however, it can also serve as an effective wealth-building tool. Unlike term life insurance, whole life policies accumulate cash value over time, which can grow at a guaranteed rate. This cash value can be accessed during the policyholder's lifetime, providing a source of funds for various financial needs, such as funding a child's education, purchasing a home, or supplementing retirement income.

Additionally, the growth of cash value in a whole life insurance policy is typically tax-deferred, meaning you won't have to pay taxes on the accrued gains until you withdraw them, if at all. This makes whole life policies a strategic choice for long-term financial planning. By leveraging the cash value through policy loans or withdrawals, individuals can create a diversified approach to wealth-building while maintaining the important life insurance coverage that protects their loved ones.